Tracing the Path from Deposit to Disbursement: Payment Options' Influence on Withdrawal Efficiency in Digital Sportsbooks and Casinos

Digital sportsbooks and casinos process millions of transactions daily, and the journey from initial deposit to final disbursement often hinges on the payment methods players select at the start. Observers note that choices made during funding directly shape how quickly funds return later, because many platforms tie withdrawal options to the original deposit channel for security and compliance reasons. Data from industry reports shows that e-wallet users frequently complete the full cycle faster than those relying on traditional bank wires, while cryptocurrency transactions introduce new variables around volatility and verification speed. Payment providers differ in their infrastructure, and these differences compound across the process. When a player deposits via an e-wallet such as PayPal or Skrill, the system records the transaction instantly and often pre-approves the reverse path. This linkage reduces verification steps later, since the account details already match. Bank transfers and credit cards, by contrast, require additional layers of confirmation that can stretch timelines from hours into days. Researchers tracking transaction logs across multiple operators have documented average withdrawal windows ranging from under 24 hours for digital wallets to five business days for wire services.

Digital sportsbooks and casinos process millions of transactions daily, and the journey from initial deposit to final disbursement often hinges on the payment methods players select at the start. Observers note that choices made during funding directly shape how quickly funds return later, because many platforms tie withdrawal options to the original deposit channel for security and compliance reasons. Data from industry reports shows that e-wallet users frequently complete the full cycle faster than those relying on traditional bank wires, while cryptocurrency transactions introduce new variables around volatility and verification speed. Payment providers differ in their infrastructure, and these differences compound across the process. When a player deposits via an e-wallet such as PayPal or Skrill, the system records the transaction instantly and often pre-approves the reverse path. This linkage reduces verification steps later, since the account details already match. Bank transfers and credit cards, by contrast, require additional layers of confirmation that can stretch timelines from hours into days. Researchers tracking transaction logs across multiple operators have documented average withdrawal windows ranging from under 24 hours for digital wallets to five business days for wire services.

Digital sportsbooks and casinos process millions of transactions daily, and the journey from initial deposit to final disbursement often hinges on the payment methods players select at the start. Observers note that choices made during funding directly shape how quickly funds return later, because many platforms tie withdrawal options to the original deposit channel for security and compliance reasons. Data from industry reports shows that e-wallet users frequently complete the full cycle faster than those relying on traditional bank wires, while cryptocurrency transactions introduce new variables around volatility and verification speed. Payment providers differ in their infrastructure, and these differences compound across the process. When a player deposits via an e-wallet such as PayPal or Skrill, the system records the transaction instantly and often pre-approves the reverse path. This linkage reduces verification steps later, since the account details already match. Bank transfers and credit cards, by contrast, require additional layers of confirmation that can stretch timelines from hours into days. Researchers tracking transaction logs across multiple operators have documented average withdrawal windows ranging from under 24 hours for digital wallets to five business days for wire services.How Deposit Methods Set Withdrawal Timelines

The initial deposit creates a digital trail that regulators and operators follow. Many platforms enforce a "same method" rule to prevent money laundering, which means a credit card deposit typically forces a credit card withdrawal even if slower alternatives exist. This policy stems from guidelines issued by bodies like iGaming Ontario, where compliance teams audit trails to ensure consistency. Players who mix methods often encounter extra documentation requests that pause processing entirely. Verification plays a central role once funds move toward disbursement. Operators cross-check identity documents against the payment source, and mismatches trigger manual reviews. E-wallet accounts usually carry pre-verified status from their own providers, which shortens this phase. Bank accounts demand fresh proof of ownership, adding friction. Figures released in May 2026 by the European Gaming and Betting Association revealed that platforms integrating automated KYC tools cut average verification time by 40 percent compared with manual systems, benefiting users who started with instant payment apps.Comparing Core Payment Categories

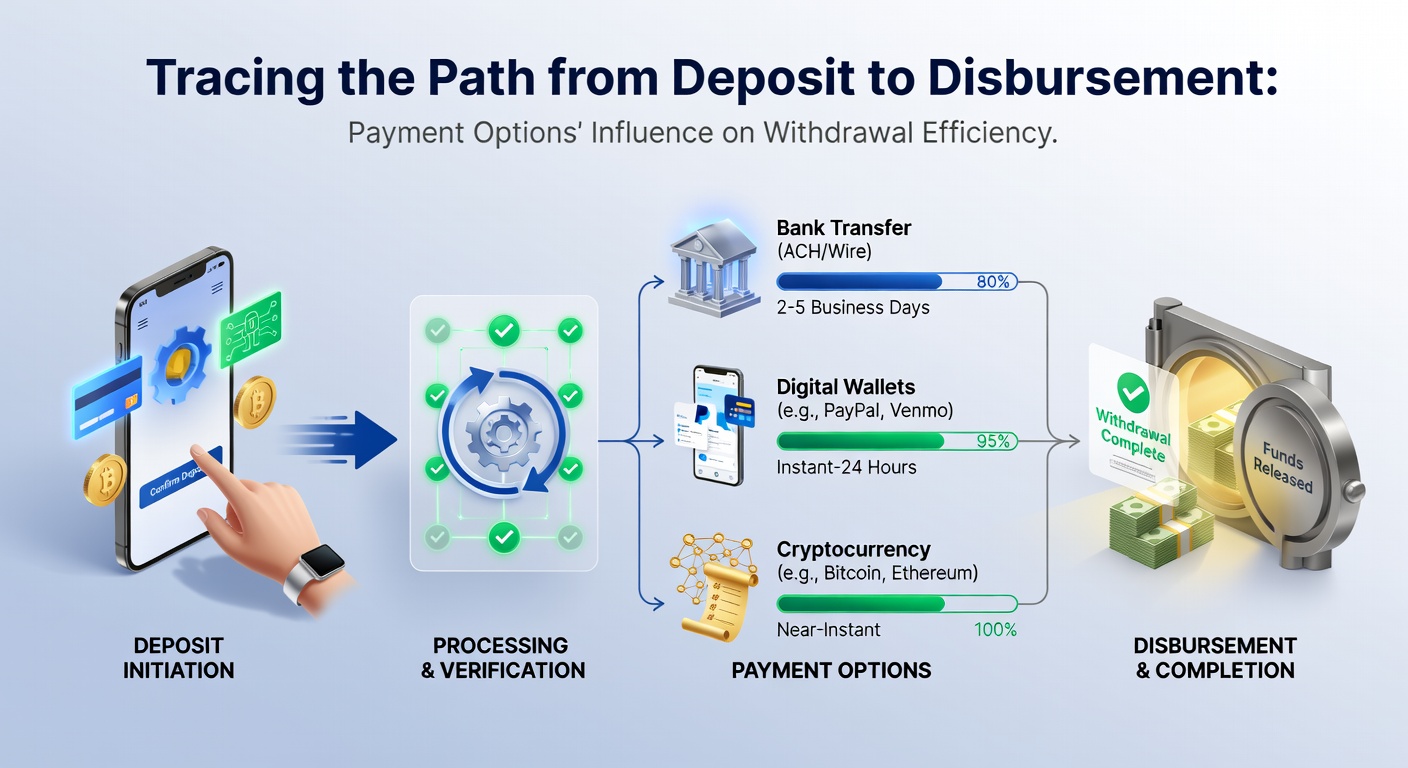

Credit and debit cards remain common entry points yet lag in return speed. Networks like Visa and Mastercard handle deposits within seconds, but cashback to the same card can take three to seven days while issuers complete their internal clearances. Some operators now offer instant card withdrawals through specialized processors, though availability stays limited to select regions and high-volume accounts. E-wallets dominate efficiency rankings. Services such as Neteller and ecoPayz process both deposits and withdrawals in minutes once initial approvals clear. Their internal ledgers allow instant transfers between user balances and operator accounts, bypassing slower banking rails. Industry analyses indicate these methods account for over 60 percent of rapid payouts on major platforms because they minimize intermediary banks. Cryptocurrency options have gained traction since regulatory clarity improved in several jurisdictions. Bitcoin and Ethereum deposits confirm on the blockchain within minutes to hours, and withdrawals follow similar patterns when networks are uncongested. Volatility remains a factor, however, as exchange rates fluctuate between deposit and payout. Operators that lock rates at transaction time reduce user exposure, and data shows growing adoption in markets where traditional banking faces restrictions. Bank transfers offer reliability for larger sums but sacrifice speed. ACH and SEPA systems settle in one to three days domestically, while international wires extend further. Players often choose these for high-value disbursements despite the wait, because limits exceed those of digital wallets. Security features built into banking protocols provide reassurance that offsets the delay for some users.